As you are probably well aware, the Australian Taxation Office (ATO) has deferred until 1 March 2022 the deadline by which all businesses in Australia must comply with requirements of phase 2 of its Single Touch Payroll scheme (STP2).

As we mentioned in our first blog on STP, the deferral reflects the ATO’s recognition that achieving compliance won’t be easy and we listed all the different kinds of information associated with payments to employees’ businesses will be required to submit.

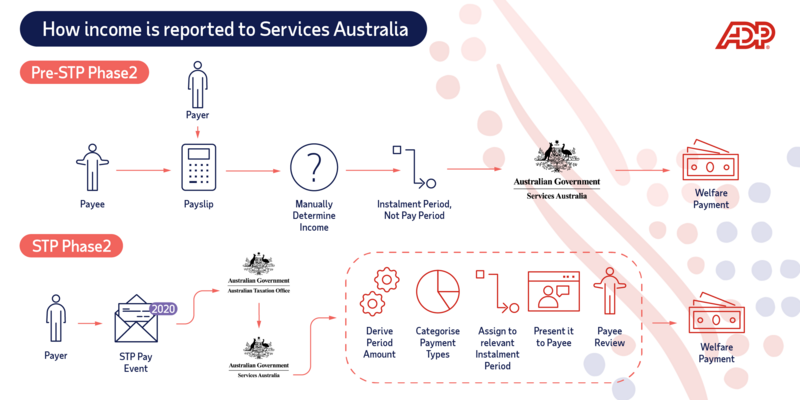

Now we’ll look at what is probably the most challenging aspect of STP2 compliance: disaggregation of gross. Because different kinds of payments to individuals are treated differently for social security purposes, the ATO wants more detail on what amounts, paid to an employee, is actually for.

The ATO uses payment data to calculate individuals’ annual tax returns. Social services agencies require income data for specific fortnightly periods in order to calculate periodic welfare payments – hence the need for a lot more detail.

The 9 disaggregated payment types

These are the 9 different kinds of payments that the ATO will require businesses to separately identify when they report employee payments to the ATO:

- Gross pay

- Paid leave

- Allowances

- Overtime

- Bonuses and commissions

- Directors’ fees

- Lump sum W (return to work)

- Lump sum E

- Salary sacrifice

Disaggregation in detail

Within each of the major categories there are, sometimes, multiple sub-categories – yes, this is getting complicated. The amounts paid under each must be correctly identified and separately reported. For example, under paid leave these are the following separately reportable categories:

- Other paid leave

- Paid parental leave

- Workers’ compensation

- Ancillary and defense leave

- Cash out of leave in service

- Unused leave on termination

While there is no requirement to separately report types of payments in some categories, there are some ‘gotchas’ (listed here) for the unwary.

New category – Lump sum W & lump sum E

Lump sum W is a new category introduced in STP Phase 2. It covers:

- A bonus paid to an ex-employee to encourage them to return to their former employer

- A bonus paid to end industrial action

- A bonus paid to encourage an employee not to resign

However, it does not include a sign-on bonus for a new employee, or payment made to an employee returning to work after being paid workers’ compensation. All other bonuses are included as standard bonuses.

Back payments may, or may not be classified as lump sum E payments, depending on the period they relate to and the amount. They are classified as lump sum E if they were accrued, or were payable, more than 12 months before the date of payment or if they exceed the lump sum E threshold of $1200.

Download our handy tool to distinguish between the lump some categories

The many bonuses and commission types

There is multiple, actually 8, kinds of bonuses and commissions:

- Christmas bonus

- Retention bonus

- Sign-on bonus for new employees

- Performance bonus

- Referral bonus

- Bonus labelled as ex-gratia but in respect of ordinary hours worked

- Return to work bonus after parental leave

- Commission payment

These individual bonus types are not required to be separately identified, but if any of these payments relate entirely to work performed outside normal hours they must be reported as overtime, not as bonuses. And not all payments paid at overtime rates should be reported as overtime. Shift penalties, for example, must be reported in gross.

Under some awards an employee required to work in what should be a mandatory rest break between shifts must be paid at overtime rates. However, these payments must be reported in gross, not as overtime.

Another tricky one is, if an employee takes cash instead of taking a rostered day off, that’s reported as cashed out leave. But if they stay back for a couple of hours and take cash instead of time in lieu, that’s reported as overtime.

Allowances

There are multiple kinds of allowances, each of which must be separately reported:

- Cents per km

- Award transport payments

- Laundry

- Overtime meal allowance

- Domestic or overseas travel

- Tool allowances

- Qualification and certification allowances (allowance type QN)

- Task allowances (allowance type KN)

- Other allowances (allowance type OD)

Download our guide that summaries all of the Allowance types and definitions.

Task allowances, a new task for you

Reporting of task allowances also represents a new task for businesses. These allowances were previously not individually identified and were reported as part of gross income. Under STP2 amounts paid under any of these categories are not reported individually but must be identified as such and reported as amounts under task allowances. Here’s the list:

- First aid allowance

- Leading hand allowance

- Higher duties or supervisor allowances

- On call during ordinary hours allowance

- Inconvenience or disability

- Height or danger allowance

- Hot or cold allowances

- Dirt or wet weather allowances

- All-purpose allowance

- Industry allowance

- Site, district, or locality allowances

- Recognition of skill level allowances

Payments to The Directors

You probably guessed it – all amounts paid to directors also need to be identified and separately reported. The fee of their services is reported as ‘director’s fees’ and is any amount paid for travel costs to attend meetings and ‘expenses related to the position of a company director’. However, any bonus paid to a director must be reported under ‘bonuses and commissions’, and any allowance for any other reason must be reported under the relevant allowance category and sub-category type.

Vehicle use allowances

Amounts to be reported as a cents per km allowance are only where those amounts relate to the use of a private car for business travel. Cents per km payments for vehicles other than a car (such as a motorbike or van) are reported as ‘other allowances > private vehicle’, and a flat rate car allowance is reported as ‘other allowances > private vehicle’.

Cents per km payments for private travel, such as travel between home and work, are generally reported as ‘other allowances > non-deductible’.

Preparing for and implementing disaggregation

So, the onus is on every organisation to review all its payments policies and procedures to make sure every kind of payment is correctly classified according to the requirements of STP2, and then correctly reported. The ATO has said it will take a fair and flexible approach to the roll out but it’s best to get it right the first time. Next year they may feel differently.

If you need more information on disaggregation of gross pay, you’ll find definitive under each payment type on the ATO website and at our resources page.